Definition of Accounting Accounting is the process of collecting economic data and information, and then processing such information through recording, classifying, and summarizing financial transactions. The results are presented in monetary terms through various forms of financial reports for use in analysis, planning, decision-making, and evaluating the financial performance of an organization.

Accounting refers to the process of collecting economic and financial information and then processing that information through recording, classifying, and summarizing transactions. The results are presented in monetary terms through various types of reports, enabling users to analyze financial performance, make informed decisions, and evaluate the financial position of a business or organization.

In this article, we will explain each of these processes in detail to help you gain a clearer understanding of what accounting means and why it plays a vital role in the management and operation of every business and organization.

What Are the Steps in Accounting (Bookkeeping)?

Accounting, or bookkeeping, consists of several key steps that form the foundation of the accounting process. These steps ensure that financial information is properly collected, recorded, processed, and reported for effective business management and decision-making. The main stages of accounting are as follows:

1. Collection of Financial Information

2. Recording Financial Transactions

3. Classification of Financial Information

4. Summarization of Financial Information

Collection of Financial Information

Accounting, or bookkeeping, begins with the collection of all financial information and transactions that affect the company's financial position. These records must be gathered completely and accurately before they can be processed through the subsequent stages of the accounting cycle.

In general, the primary types of information and documents that should be collected include the following:

1. Sales Information and Supporting Documents

2. Cash Receipt Information and Supporting Documents

3. Purchase Information and Supporting Documents

4. Payment Information and Supporting Documents

5. Fixed Asset Information and Supporting Documents

6. Inventory Information and Supporting Documents

7. Employee Information and Supporting Documents

Recording Financial Transactions

In accounting systems, financial transactions are recorded using the Debit (Dr.) and Credit (Cr.) method, which is a globally accepted standard for bookkeeping. This system may be slightly difficult to understand for those without an accounting background.

In general, it can be summarized as follows:

1. Assets Increase – Debit (Dr.)

2. Assets Decrease – Credit (Cr.)

3. Liabilities Increase – Credit (Cr.)

4. Liabilities Decrease – Debit (Dr.)

5. Owner’s Equity Increase – Credit (Cr.)

6. Owner’s Equity Decrease – Debit (Dr.)

7. Revenue Increase – Credit (Cr.)

8. Revenue Decrease – Debit (Dr.)

9. Expenses Increase – Debit (Dr.)

10. Expenses Decrease – Credit (Cr.)

In the recording stage, all documents and transaction data collected from the previous step are used to record accounting entries. These transactions are then entered into the accounting system using the Debit (Dr.) and Credit (Cr.) format in the journal (general journal).

This process ensures that every business transaction is properly recorded in a structured and systematic manner, forming the basis for further classification, posting to ledgers, and preparation of financial statements.

Types of Journals (Books of Original Entry)

A journal entry in the accounting system typically contains key details that ensure each transaction is properly recorded and traceable. These include the company name, the date of the transaction, the account code, the account name, the debit amount, the credit amount, and a description of the transaction.

In the recording stage, various types of journals (books of original entry) are used depending on the nature of transactions involved. Each journal is designed to help organize and record specific types of financial activities accurately and systematically.

The main types of journals involved are as follows:

- Sales Journal – A record used to record sales transactions of the business

- Cash Receipts Journal – A record used to record cash inflows of the business

- Purchase Journal – A record used to record the business’s purchase transactions

- Cash Payments Journal – A record used to record cash outflows of the business

- General Journal – A record used to record transactions not included in specialized journals

Classification of Financial Information

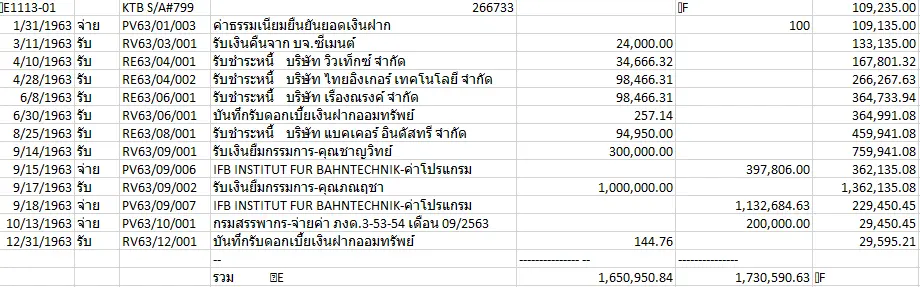

After completing the recording of accounting transactions, the next step is to classify the recorded data in order to prepare the general ledger. This process allows the organization to understand the movement of each account, including increases, decreases, and changes, as well as the source of each transaction and supporting document.

The image shows an example of a general ledger for the bank deposit account. It illustrates the increases and decreases in the company’s bank balance resulting from daily receipts and payments of various transactions.

Each entry includes a reference document number, which allows users to trace back to the supporting documents used in the original accounting entries. This makes it possible to verify and review the source documents by referring to the general ledger report, ensuring transparency and accuracy in the accounting system.

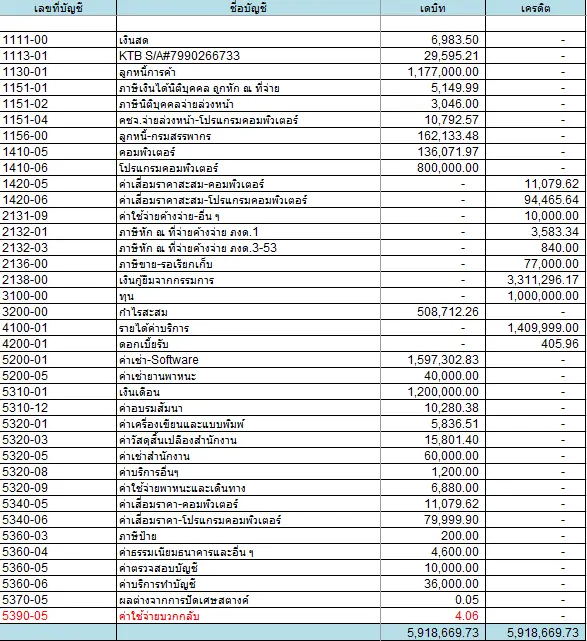

Summarization of Financial Information

After completing the classification of financial data, the next step is to summarize the information by taking the ending balances from each account in the general ledger. These balances are then used to prepare the trial balance.

An example of a trial balance is shown below:

The trial balance obtained from the previous step is then further grouped into financial reporting categories to prepare the financial statements. This process involves reorganizing account balances into structured financial reports that provide a clear view of the organization’s financial position and performance.

The financial statements are generally classified as follows:

1. Statement of Financial PositionThe Statement of Financial Position (also known as the Balance Sheet) is a financial statement that shows the financial position of a company at a specific point in time, such as 31/12/64.

It presents the company’s assets, liabilities, and shareholders’ equity, allowing users to understand what the company owns, what it owes, and the residual interest of the owners at that particular date.

2. Income StatementThe Income Statement is a financial statement that shows the company’s operating performance over a specific period of time, such as from 01/01/64 to 31/12/64.

It reports the company’s revenues, expenses, and net profit or loss, allowing users to evaluate how effectively the business has generated income and controlled its costs during the accounting period.

3. Statement of Changes in EquityThe Statement of Changes in Equity is a financial statement that shows the changes in shareholders’ equity over a specific period of time.

It explains how the equity of the owners has changed during the accounting period due to factors such as profit or loss, additional investments, dividends, and other adjustments that affect the owner’s interest in the business.

4. Statement of Cash FlowsThe Statement of Cash Flows is a financial statement that shows the cash inflows and cash outflows of a business over a specific period of time.

It provides information on how much cash the company has received and paid during the period, as well as how the cash was used in operating, investing, and financing activities. This statement helps users understand the company’s liquidity and cash management performance.

5. Notes to Financial StatementsThe Notes to Financial Statements provide additional explanations and details that support the information presented in the financial statements, making them clearer and more understandable.

They typically include general information about the company, the nature of its business, accounting policies applied by the company, and detailed breakdowns of individual accounts within the financial statements. These notes help users gain a deeper understanding of the financial position and performance of the business.

Conclusion: What Is Accounting?

After reading this article, we now understand that accounting refers to the process of collecting various economic data and processing it through recording in journals, classifying, and summarizing the information into monetary form. This is then presented in different types of financial reports, such as the trial balance and the general ledger.

Some people may wonder what “accounting” means. In fact, accounting has the same meaning as “accounting,” which refers to the systematic process of collecting economic data and processing it through recording, classifying, and summarizing it into monetary information that is presented in various forms of financial reports.

The financial reports produced through accounting are intended for users who need to analyze and interpret financial information. For example, company owners use financial statements to understand the financial position and performance of their business in order to support strategic planning and decision-making.

The Revenue Department uses financial statements to assess tax-related matters of the company. Banks also rely on financial statements to evaluate the creditworthiness of borrowers when considering loan approvals. In this way, financial reports serve as an important tool for various stakeholders in making informed decisions.